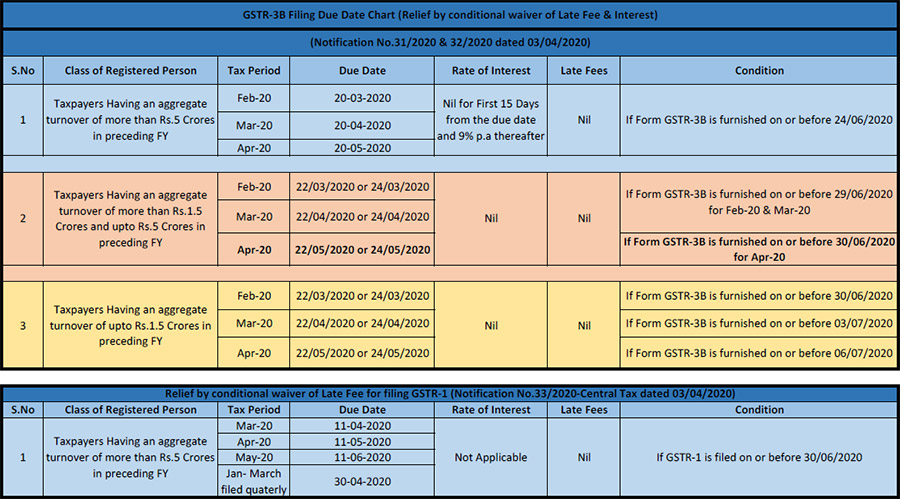

Income Tax Act

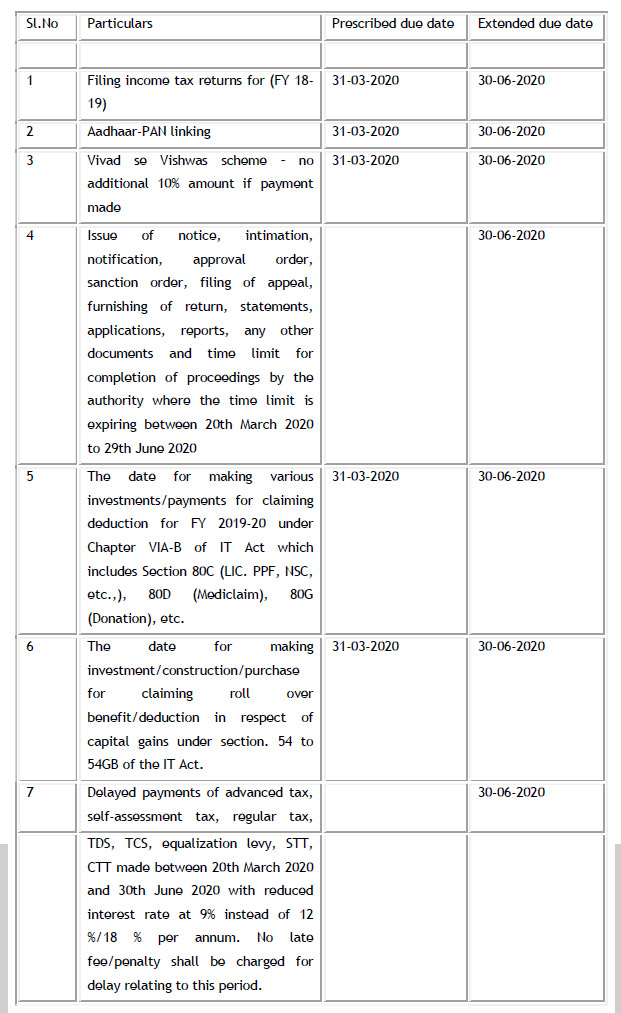

1. Extension of due dates and relief measures in view of COVID-19 outbreak.

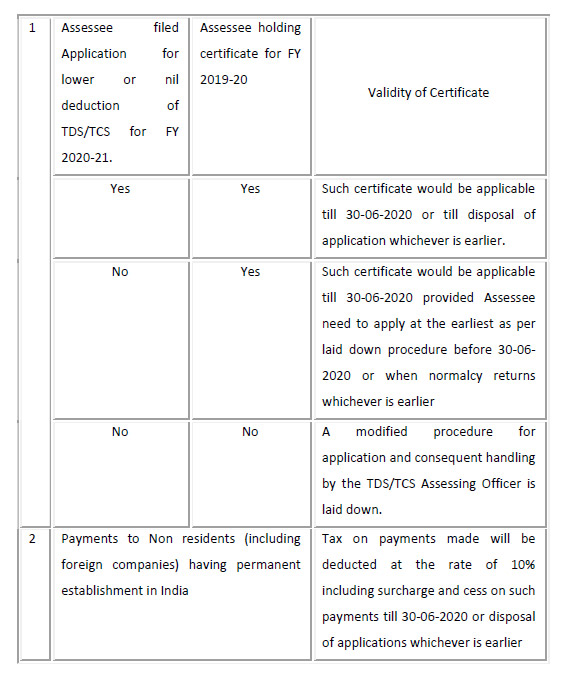

2. Relaxation in issuing certificates for lower rate/nil deduction/collection of TDS or TCS u/s 195, 196 and 206C(9) of Income Tax Act.

3. Relaxation with respect to short deduction of TDS/TCS due to increase in rates of surcharge by Finance Act 2019

It is clarified a person responsible for deduction/collection of tax under any provision of the Income-tax Act will not be an assessee in default in respect of transactions where

- Such transaction has been completed and entire payment has been made to the deductee/payee on or before 5th July, 2019 and there is no subsequent transaction between the deductor/collector and the deductee/payee in the financial year 2019-20 from which the shortfall of tax could have been deducted/collected by the deductor/collector.

- TDS has been deducted or TCS has been collected by such deductor/collector on such sum as per the rates in force as per the provisions prior to the enactment of the Act.

- Such tax deducted or collected has been deposited in the account of Central Government by the deductor/collector on or before the due date of depositing the same.

- TDS/TCS statement has been furnished by such person on before the due date of filing of the said statement.

4. Clarifications on provisions of Direct Tax Vivad se Vishwas Act, 2020

55Questions contained in circular no 7 of 2020 are reissued under this circular with following modifications

(i) Vivad se VishWas referred to Direct Tax Vivad se Vishwas Bill, 2020 in circular no 7. However, in this circular it refers to The Direct Tax Vivad Se Vishwas Act, 2020;

(ii) Since clauses of the Bill have now become sections in the Vivad Se Vis/lWas, the reference to “clause” in circular no 7 has been replaced with “section”;

(iii) Reference to declaration form in circular no 7 has been replaced with referencing of relevant fonn, since rules and forms have now been notified; and

(iv) Answer to question no 22 has been modified to reflect the correct intent of the law. It has now been clarified that where only notice for initiation of prosecution has been issued without prosecution being instituted, the assessee is eligible to file declaration under Vivad se Vishwas. However, where the prosecution has been instituted with respect to an assessment year, the assessec is not eligible to file declaration for that assessment year under Vivad se Vishwas, unless the prosecution is compounded before filing the declaration.

(v) Section 10 and II of the Vivad se Vishwas empowers the Board or the Central Government to issue directions or orders in public interest or to remove difficulties. This circular is such direction/order issued under section 10 and section II of the Vivad se Vishwas. Thus answers to some of the questions in this circular extend the application of Vivad se Vishwas in public interest or to remove difficulties, under section 10 and section II of Vivad Se Vishwas

5. Government to release IT Refunds

6. Clarification in respect of option under section 115BAC of the Income-tax Act, 1961

An employee, having income other than the income under the head “profit and gains of business or profession” and intending to opt for the concessional rate under section 115BAC of the Act, may intimate the his employer, of such intention for each previous year and upon such intimation, the deductor shall compute his total income, and make TDS thereon in accordance with the provisions of section 115BAC of the Act.

If such intimation is not made by the employee, the employer shall make TDS without considering the provision of section 115BAC of the Act. The intimation would not amount to exercising option in terms of Section.115BAC(5) of the Act and the person shall be required to do so along with the return to be furnished under sub-section (J) of section 139 of the Act for that previous year.

Further a person who has income under the hcad “profit and gains of business or profession” also, the option for taxation under section 115BAC of the Act once exercised for a previous year at the time of filing of return of income under section.139(1) of the Act cannot be changed for subsequent previous years except in certain circumstances.

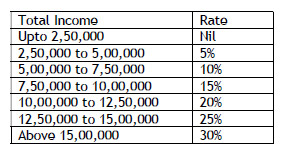

Abstract of Section. 115BAC of the Income Tax Act:

New Slab rate for Individuals

Exemption or Deduction not available for:

1. Leave travel concession – Section. 10(5)

2. House Rent Allowance – Section. 10(13A)

3. Exempted allowances so far – Section. 10(14)

4. Allowance received by MP/MLA – Section. 10(17)

5. Income of Minor – Section. 10(32)

6. Standard deduction & Professional Tax paid – Section.16

7. Interest on borrowed capital for house property – Section. 24(b)

8. Additional Depreciation on Plant and Machinery – Section. 32(1)(iia)/32AD

9. Specified Investment allowance

10. One third deduction from family pension – Section. 57(iia)

11. Deduction under Chapter VIA except in contribution to pension scheme (Sec. 80CCD) and

deduction in respect of employment of new employees (Sec. 80JJAA)

12. No carried forward of House Property Loss

COMPANIES ACT

7. Special Measures under Companies Act, 2013 (CA-2013) and Limited Liability Partnership Act, 2008 in view of COVID-19 outbreak

In order to support and help the Companies and Limited Liability Partnerships in India to focus on taking measures to address the COVID-19 threat and revive themselves from economic disruptions caused by it, the Ministry of Corporate Affairs (MCA) has taken some measures by reducing certain compliances under the Companies Act, 2013 on the Corporates. The details of the reliefs provided by MCA are explained as under:

- No additional fees shall be charged for late filing of any documents, return etc. with MCA during the period from April 01, 2020 to September 30, 2020.

- The requirement of holding board meetings within prescribed interval of 120 days, stands extended by a period of 60 days till next two quarters i.e., till 30th September. Accordingly, as a one-time relaxation the maximum gap between 2 consecutive board meetings may extend upto 180 days, till September 30, 2020.

- The Companies (Auditor’s Report) Order, 2020 shall now be applicable from the financial year 2020-2021 instead of 2019-2020.

- In case the independent directors could not hold their meeting during the financial year 2019-2020, the same shall not be treated as non-compliance or violation of the Companies Act, 2013.

- Requirement of creating the deposit repayment reserve under section 73(2)(c) of the Companies Act, 2013 for the financial year 2020-2021 on or before April 30, 2020 has been extended till June 30, 2020. The aforesaid requirement is applicable on the companies accepting deposits from its members after obtaining the approval from its shareholders. It includes depositing the amount which shall not be less than 20% of the amount of its deposits maturing during the following financial year and to be kept in a scheduled bank account separately to be called deposit repayment reserve account.

- Requirement of investing or depositing certain amount of debentures maturing in specified methods of investments or deposits as per rule 18 of the Companies (Share Capital & Debentures) Rules, 2014 on or before April 30, 2020 has been extended till June 30, 2020.

- Every newly incorporated company are required to file a declaration in form INC-20A within 180 days from the date of its incorporation stating that every subscriber to the memorandum has paid the value of the shares agreed to be taken by him. MCA has now provided an additional time limit of 180 days for filing of the aforesaid declaration. It means all the newly incorporated companies can file form INC-20A within a period of 360 days from the date of its incorporation.

- Requirement of having at least one director in a company qualifying as resident in India as per section 149(3) of the Companies Act, 2013 has been waived off for the financial year 2019-2020. It means in case any company fails to have at least one resident director on its Board of directors during the financial year 2019-2020 then the same shall not be treated as non-compliance.

View PDF

8. MCA Clarification on passing of Ordinary and Special Resolution on account of threat posed by Covid-19

The Ministry of Corporate Affairs vide circular dated 8th April, 2020 has permitted companies to conduct Extra-ordinary General Meetings (EGM) of the Members of the company for discussing urgent matters upto 30th June 2020 through Video Conference (VO) or Other Audio Visual Means (OAVM).

Further, the Ministry of Corporate Affairs vide its circular dated 13th April, 2020 has clarified and issued detailed framework for conducting the Extra-ordinary General Meetings by the Companies through Video Conference (VO) or Other Audio Visual Means (OAVM) in prescribed manner.

9. Settlement Scheme 2020 introduced for Companies and Limited Liability Partnership

1.In pursuance of the Government of India’s efforts to provide relief to law abiding companies and Limited Liability Partnerships (LLPs) in the wake of COVID 19, the Ministry of Corporate Affairs, has introduced the “Companies Fresh Start Scheme, 2020” and revised the “LLP Settlement Scheme, 2020” which is already in vogue to provide a first of its kind opportunity to both companies and LLPs to make good any filing related defaults, irrespective of duration of default, and make a fresh start as a fully compliant entity. The Fresh Start scheme and modified LLP Settlement Scheme incentivize compliance and reduce compliance burden during the unprecedented public health situation caused by COVID-19. The USP of both the schemes is a one-time waiver of additional filing fees for delayed filings by the companies or LLPs with the Registrar of Companies during the currency of the Schemes, i.e. during the period starting from 1st April, 2020 and ending on 30th September, 2020.

2. The Schemes, apart from giving longer timelines for corporates to comply with various filing requirements under the Companies Act 2013 and LLP Act, 2008, significantly reduce the related financial burden on them, especially for those with long standing defaults, thereby giving them an opportunity to make a “fresh start”. Both the Schemes also contain provision for giving immunity from penal proceedings, including against imposition of penalties for late submissions and also provide additional time for filing appeals before the concerned Regional Directors against imposition of penalties, if already imposed. However, the immunity is only against delayed filings in MCA 21 and not against any substantive violation of law.

3. Details of the both the Schemes may be perused from the Circulars dated 30.03.2020 and list of e-forms for eligible for additional fee waiver under Companies Fresh Start Scheme 2020 and the LLP Settlement Scheme 2020, issued by the Ministry of Corporate Affairs.

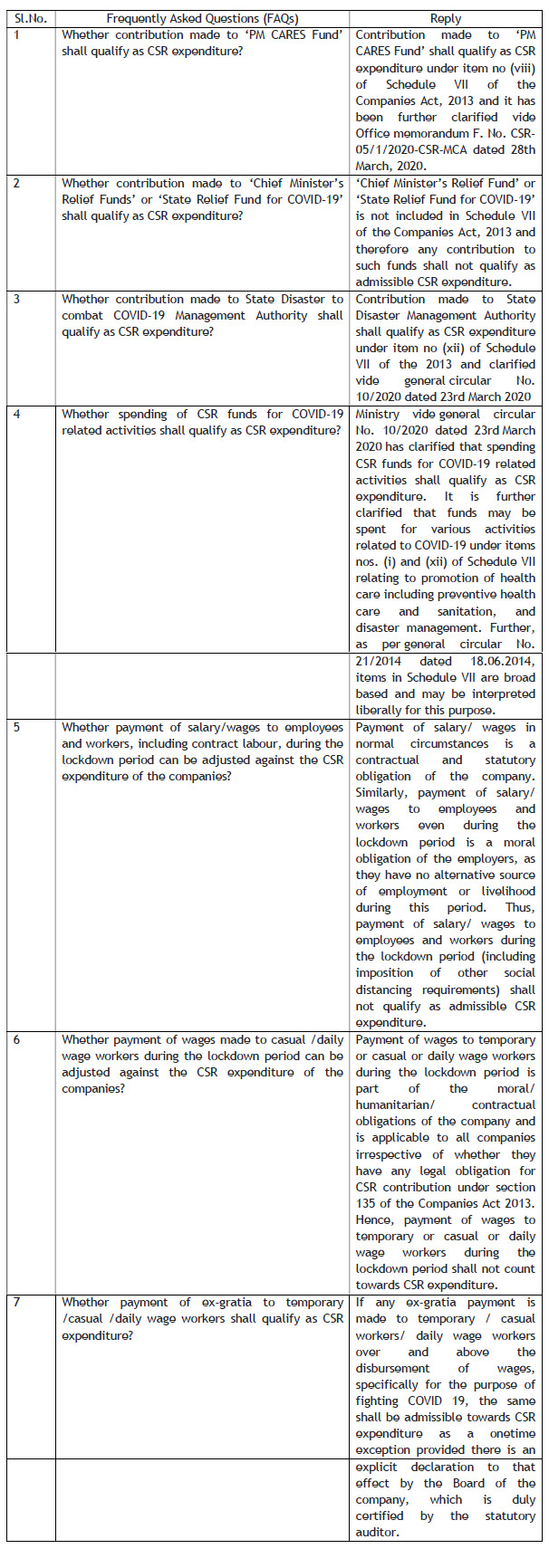

10. MCA Clarification On Spending Of CSR Funds And Other Relief Measures Due To COVID-19 Outbreak

In light of the ongoing COVID-19 pandemic outbreak, the Ministry of Corporate Affairs (the “MCA”) on March 23, 2020 has clarified that spending CSR funds for Covid-19 is also qualify as CSR expenditure (including of PM Cares funds) under the Companies Act 2013. Furth MCA vide its another circular dated 10th April 2020 have issued FAQ form of clarification on CSR Spending on Covid -19. The FAQ issued by MCA on CSR Spending for Covid -19 is furnished below.